The digital revolution has changed the way we consume goods and services, how we engage with our mobile devices, and what we expect from the companies we consume from.

Meanwhile, the consumer digital banking revolution has changed what we expect in terms of nicely designed banking platforms, cheaper services, and easier access to an array of banking products and services.

Regardless of product or customer segment, when I think about the next logical step in these revolutions, I think about how innovators can make services more personalised and relevant with an even greater focus on the customer. In order to do this, lenders will need to focus on utilising data in smarter ways.

Within the broader financial services revolution, there are a handful of players that are already using data in a smart way, both from a “what do we do with this” and a “how do we obtain this” perspective. As we continue to explore the nuances of the SME lending area, this article will highlight smart uses of data that innovators in the SME lending area can look to for inspiration.

Klarna: disrupting the credit space

Klarna has changed the way in which consumers pay online and how sellers manage payments of their goods and services. There is a whole host of learnings to take from Klarna, but we will focus on a recent acquisition by the Swedish Bank and valuation unicorn.

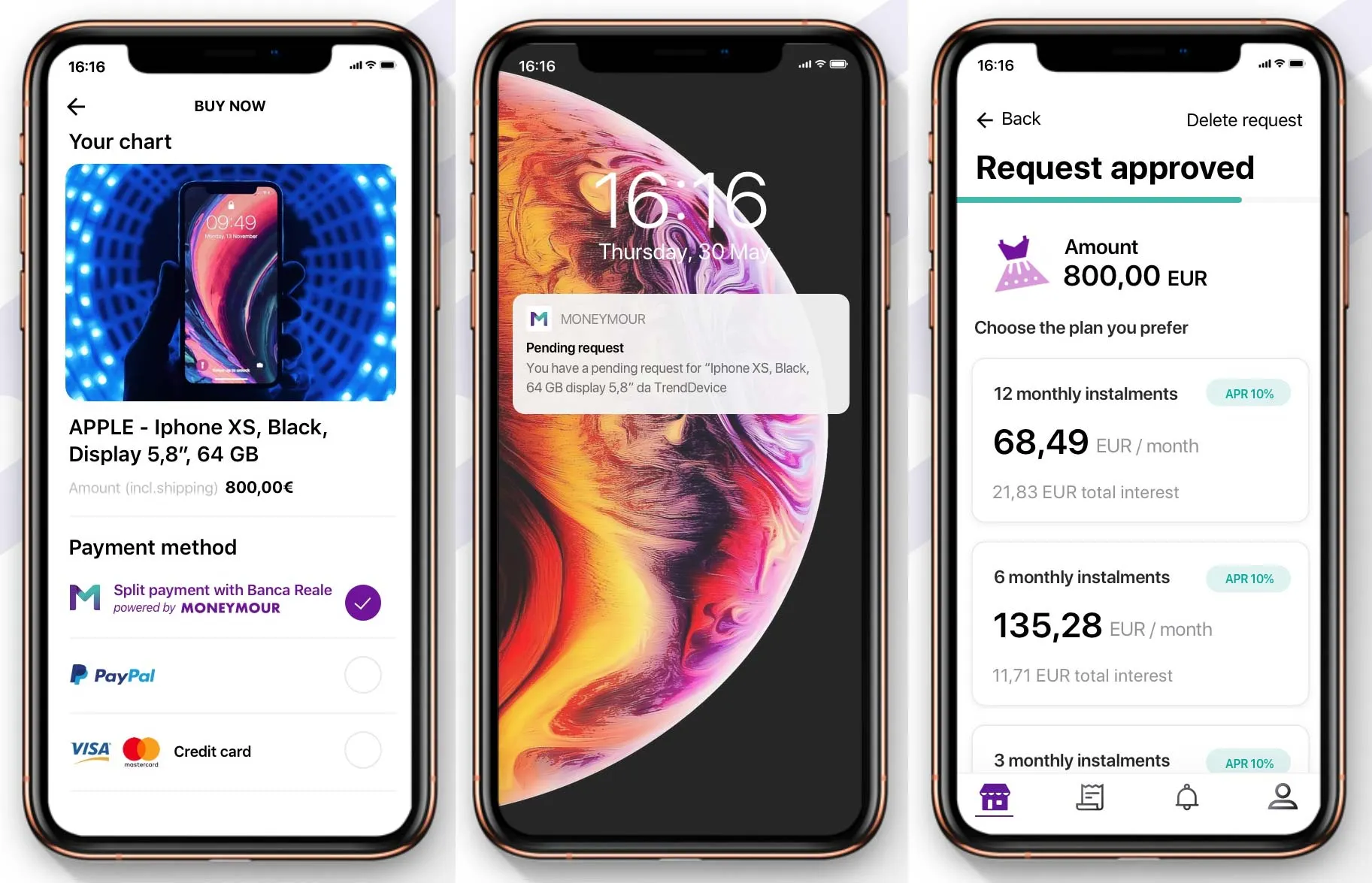

Recently Klarna purchased Italian firm Moneymour. Moneymour was founded in 2017 and enables consumers to split their purchases into monthly instalments based on an instant credit assessment that uses balance and transaction data from Open Banking feeds in the credit scoring algorithm.

Customers select Moneymour at the checkout page, and if approved, select the instalment plan they prefer. The Open Banking part comes in as the customer provides Moneymour with read-only access to their transactions, where previously customers would have to manually send account statements in order to receive approval for a loan.

As part of the acquisition, Klarna has taken over the intellectual property rights to Moneymour’s scoring engine and will integrate it into the markets it currently operates in. Klarna acquired the intellectual property rights to Moneymour’s scoring engine, indicating there is something very attractive in their secret sauce for how they ascertain credit worthiness. The credit scoring capabilities and value proposition can easily be applied to the SME lending space. Two potential use cases could be:

An unplanned, large purchase comes up for an SME. Also, three out of five customers have not paid their invoices on time. Rather than the SME feeling the pinch, the instalment payments can ease the potential financial pain

SMEs such as coffee shops, restaurants, or hospitality that require large, but not full-loan worthy purchases such as furniture or equipment when opening up a new store.

This approach would likely be highly attractive to SMEs, especially those who have been operating for a short period of time, because Klarna offers payment finance options even if customers do not have a credit history and instalment payments do not impact the credit score: A potential win-win for SMEs.

The learning here is that the future will be all about using the right data fast in order to quickly fulfil lending requirements.

Screens from Moneymour

Taking a Chip out of the micro-savings players

The likes of Chip, Oval Money, and Acorns have all revolutionised the savings space for consumers. By facilitating micro-savings with minimal customer input, they have collectively helped thousands of—primarily young—people begin to grow their savings and investment portfolios. Each uses a variety of tactics, from round-ups to clever algorithms to figure out how much a user can save each week based on spend, or spend and fitness-driven rules.

Some of these tactics can be applied to the SME lending space. For example, lenders can use AI to understand business spending and if there is a week with less expenses and greater income, they can then suggest that the business puts that extra cash towards an outstanding loan.

While the obvious criticism is that this isn’t necessarily in the interest of the lender financially, as they would want to earn interest from the loan, it aligns with the growing need for customer centricity in financial services, given the increasing pressure from GAFA/Big Tech and mobile-first disruptors. In the longer term, this approach will certainly achieve a greater customer lifetime value.

The learning here is that understanding businesses’ spend and cashflow can help them with outstanding loans via micro-payments.

Outside of financial services: the data ownership revolution

Thinking about data in a broader sense, it's important to consider the quiet revolution happening, in particular with the platforms that are looking to give data ownership back to the “rightful owners”, i.e. the individual consumer. One of which is the Solid Project, run by Sir Tim Berners-Lee, the inventor of the World Wide Web. The mission of Solid is to create a set of conventions and tools for building decentralised social applications based on Linked Data principles. This will allow individuals to do two things:

Have the freedom to choose where their data resides and who is allowed to access it. This is done by decoupling content from the application itself.

Avoid vendor lock-in, seamlessly switching between apps and personal data storage servers, without losing any data or social connections.

Solid is looking to flip the rules of who gets value from the data, and enjoy the benefits associated with personal data in any way that the individual sees fit. Should Solid gain momentum, and this idea of putting data back in the hands of the individuals takes off, this would heavily impact the existing model of SME lending, as data sources could dry up.

The inspiration here for SME lenders could be to take a more personalised approach to lending, working with the business to utilise the right data and re-balance the way in which we exchange data.

The future of SME lending

The SME lending space is ripe for new types of innovation, and a—if not the—key driver will be if data is used in a more clever way. The three main components to consider are how can lenders quickly obtain the right data, how can lenders use the data they have in an intelligent way, and how can lenders take a more data-friendly approach to engaging businesses.

Existing lenders should look to their counterparts in the consumer world, in particular how data can fuel new lending services that play in the micro-lending space. Open Banking initiatives are gaining traction in consumer banking, which also can provide an array of inspiration to lenders to tackle the speed of which data can be utilised. Finally, lenders could keep an eye on the players currently on the fringe looking to revolutionise the data space.

Photography: Diego PH on Unsplash